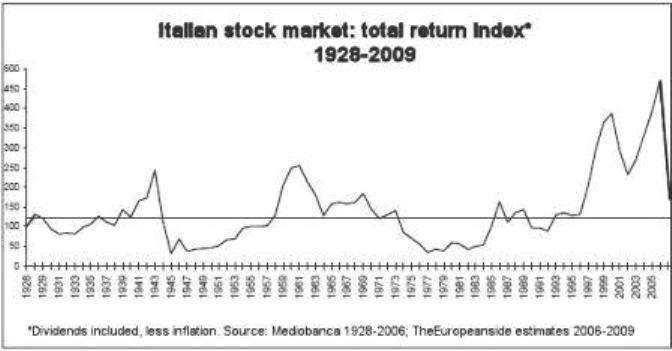

Italian stocks below the 1943 and 1960 tops

If you believe that Wall Street is cheap

because the Dow Jones Industrial Average touched the mid-1990s levels,

what about Italy, whose stock market is below the 1943 top, when Benito

Mussolini planned

to

conquer the world along with his fellow-friend Adolf Hitler?

(Click the chart to enlarge).

to

conquer the world along with his fellow-friend Adolf Hitler?

(Click the chart to enlarge).

The chart in page depicts how deep and how devastating the bear market is in real terms. It is based on data provided by Mediobanca from 1928 to 2006 and on TheEuropeanSide's estimates afterward. The chart is "total return", namely it is inflation adjusted and includes dividends.

As you can see, the March selling climax pushed the Italian stock market well below the top of 1943

- when Italy was on the

verge of the II World War disaster - and well

below the top of 1960 – after a decade of roaring years when Italy

emerged as a good industrial power. According to our calculations, the

March bottom was 20-30% below the tops of 1943 and 1960.

Another long-term historical series is provided by the Comit index,

which goes back to 1972, when it was set equal to 100. Inflation

adjusted, the index was worth 50 at the bottom of March, with a huge and

disappointing long-term loss. If you add dividends, the index was

instead worth about 140, with an annual performance of just less than 1%

per year. Of course, if you include realistic transactional costs and

capital gains, the performance veers once again into a deep negative territory.

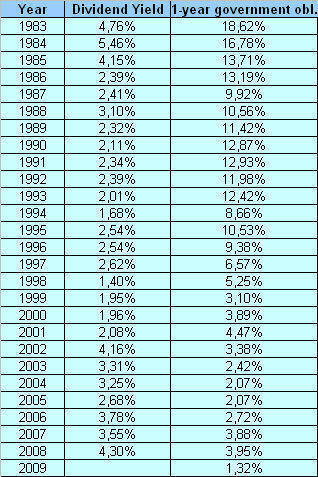

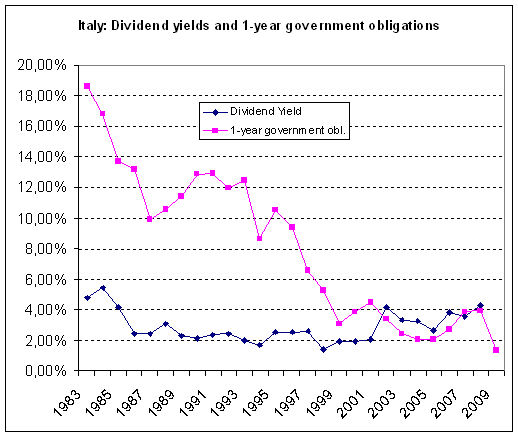

Equally important is the role of interest rates and dividend yields. At the March bottom, the value of the

Italian stock market (dividends

included) was roughly at the same

point where it was in 1986. But at the time, interest rates exerted much greater competition to stocks.

One-year government obligations yielded at the time 13.9%, well in excess of the

dividend yield, which was 2.4%.

Now the pendulum has

swung to the other extreme: one-year government

obligations yield 1.4%, while dividend yields are much greater. Until a

few days ago, Bloomberg consensus estimates indicated a 2009 dividend

yield of some 9%, which is as misleading as anything coming out of the

analyst community during the last few years, but cut it in half and the dividend

yield remains substantial and competitive.

swung to the other extreme: one-year government

obligations yield 1.4%, while dividend yields are much greater. Until a

few days ago, Bloomberg consensus estimates indicated a 2009 dividend

yield of some 9%, which is as misleading as anything coming out of the

analyst community during the last few years, but cut it in half and the dividend

yield remains substantial and competitive.

Talking to the few investors who more or less survived in good shape to

the stock bear market carnage, some are starting to accumulate,

according to what TheEuropeanSide knows. The idea is not to look for the

bottom, but to build up a long-term position over the next few months.

The wildest dream? That during the summer, traditionally a weak season

for stocks, the market suffers a new selling climax, providing a

lifetime opportunity to buy.